Going into college, I did not think about minimizing my own future

income risk because, let’s face it, I was young. But my parents, on the other

hand, definitely had that on their minds: they completely covered the cost of

my college education so that I would be debt free upon graduation. Given that

I’m an out-of-state student, that is no small cost. With the same thoughts

toward my future, my parents suggested I major in electrical engineering, where

the technical skills and know-how I would learn would make it very easy to find

good employment. Even though I had my reservations, I agreed, knowing that they

were right (as usual). I was semi-interested in technology to begin with so I

thought electrical engineering might work out for me. But even though I was a

fine student, my interest waned as I had to trudge through the basic courses where it’s

rote learning and memorization. Even though we had labs, they weren’t very

hands on, or interesting to be frank. So I decided to switch into economics,

where I have greater passion for my studies and academics. Previously, I’ve

interned at a large financial corporation with the hopes of possibly working

there in the future. I’ve also founded and led the Illini Investment Group as

an extracurricular activity. I’ve done these activities all with the hopes of

them correlating directly into the job market or, alternatively, graduate

school. I know that a career in economics, either through employment or

graduate school will offer me two good paths toward decreasing and better

managing future income risk. In a similar vein, even though I do not have an

older sibling, my older cousin is in medical school and he does have an

interest in medicine, yes, but it was also done with an eye towards a

successful career and decreasing future income risk.

Friday, September 27, 2013

Sunday, September 15, 2013

My Experience with Organizations and Transaction Costs

I'm the president of an organization on campus called the Illini Investment Group. Every Wednesday, when we meet we talk about the financial markets, business news, and facets of the financial world, like stocks and bonds to options and derivatives. I founded IIG in the Spring of 2011 and we were operational the fall of the following semester. Founding an organization and trying to lead it is an immense responsibility and task. The first order of business was to find partners, or an "executive board", not in the least because the university required it for my organization to exist in the first place.

Since I started my organization so early, there haven't been any leadership changes per se. I have remained on board as President and the two other people who I recruited as Treasurer and Tech Chair/Webmaster have also stayed on since the beginning. We have only made additions to our team, adding a Vice President as well as a board member specializing in Economics and its theory applied to real world finance. So we went through some changes in terms of adding members to the exec board, but we also went through other changes. In the beginning, the first year we were active, we didn't have any fees or dues. We wanted it to be a free, open club so that our members could completely enjoy it without incurring any costs. We quickly realized, however, that our options for social activities, like movie & pizza nights or game nights, outside our meetings every week were limited if we did not have some income to spend on extracurricular outings. Even the SORF office can only provide so much funding, especially if we wanted to do something like a trip to Chicago for a day. I used to be against dues because I thought paying was unnecessary but after spearheading this organization, my views have changed. Every enterprise has some sort of expenses and even though us exec members aren't paid, we still need some funds for the payment of equipment or bowling/billiards, and other activities in that vein.

I have also had experience interning at a large financial company for a couple summers. It is a historic and venerable firm, but it is also a very complicated organization that requires thousands working in management. As one can imagine, it is also steeped in bureaucracy (through no fault of its own). A start up or new company is quick, nimble, and agile, able to respond to market changes easily and is groundbreaking or industry-shifting in some way, especially technology companies. But as time goes on, and the company hires more and more personnel, layers of bureaucracy and "management" that weren't there before suddenly appear and take up time, money, and other resources. This phenomenon can be seen across industries where phrases like "corporate behemoth" to describe Microsoft, Exxon, Walmart are regularly used. (As a side note, at least none of these companies are as bad as the U.S. government in terms of bureaucracy.) Maybe some companies can survive this, but adding layers of bureaucracy and becoming a huge organization is a double-edged sword, especially for tech companies: it is a testament to their success but could also lead to their downfall as younger, savvier start ups create products, services, processes or technologies that disrupt and displace established ones.

I point all this out because I feel like organizational structures inherently lend themselves to transaction costs through bureaucracy and red tape - any (economic) inefficiency is a transaction cost. Time, money, and resources are being used up in ways they shouldn't be but seeing as human beings make up these organizations, that is only to be expected. Perhaps the best way to deal with this is to just simply minimize bureaucracy, red tape, and any other inefficiencies as much as humanly possible. If left unchecked, these inherent transaction costs can be dangerous.

Since I started my organization so early, there haven't been any leadership changes per se. I have remained on board as President and the two other people who I recruited as Treasurer and Tech Chair/Webmaster have also stayed on since the beginning. We have only made additions to our team, adding a Vice President as well as a board member specializing in Economics and its theory applied to real world finance. So we went through some changes in terms of adding members to the exec board, but we also went through other changes. In the beginning, the first year we were active, we didn't have any fees or dues. We wanted it to be a free, open club so that our members could completely enjoy it without incurring any costs. We quickly realized, however, that our options for social activities, like movie & pizza nights or game nights, outside our meetings every week were limited if we did not have some income to spend on extracurricular outings. Even the SORF office can only provide so much funding, especially if we wanted to do something like a trip to Chicago for a day. I used to be against dues because I thought paying was unnecessary but after spearheading this organization, my views have changed. Every enterprise has some sort of expenses and even though us exec members aren't paid, we still need some funds for the payment of equipment or bowling/billiards, and other activities in that vein.

I have also had experience interning at a large financial company for a couple summers. It is a historic and venerable firm, but it is also a very complicated organization that requires thousands working in management. As one can imagine, it is also steeped in bureaucracy (through no fault of its own). A start up or new company is quick, nimble, and agile, able to respond to market changes easily and is groundbreaking or industry-shifting in some way, especially technology companies. But as time goes on, and the company hires more and more personnel, layers of bureaucracy and "management" that weren't there before suddenly appear and take up time, money, and other resources. This phenomenon can be seen across industries where phrases like "corporate behemoth" to describe Microsoft, Exxon, Walmart are regularly used. (As a side note, at least none of these companies are as bad as the U.S. government in terms of bureaucracy.) Maybe some companies can survive this, but adding layers of bureaucracy and becoming a huge organization is a double-edged sword, especially for tech companies: it is a testament to their success but could also lead to their downfall as younger, savvier start ups create products, services, processes or technologies that disrupt and displace established ones.

I point all this out because I feel like organizational structures inherently lend themselves to transaction costs through bureaucracy and red tape - any (economic) inefficiency is a transaction cost. Time, money, and resources are being used up in ways they shouldn't be but seeing as human beings make up these organizations, that is only to be expected. Perhaps the best way to deal with this is to just simply minimize bureaucracy, red tape, and any other inefficiencies as much as humanly possible. If left unchecked, these inherent transaction costs can be dangerous.

Thursday, September 12, 2013

The Fine Line Between Academic Integrity and Opportunism

In terms of college, I think the biggest opportunism factor is that in homework and exams. College students regularly find creative ways to circumvent the ideal homework process as perceived by the instructor: each individual diligently does his (or her) homework assignment by himself without any outside help (unless it's a group assignment), all the while learning the concepts and theories taught in class and valuable life lessons in time management - that hard work is its own reward. While all of that is true and would be the best case scenario for both the student and the professor, in reality, students often engage in these creative ways to bypass that whole arduous and time-consuming process.

Students might often collaboratively work in groups when the assignment does not call for it, and while they may not always copy each other's work word for word, it is still not strictly ethical behavior. But what is ethically worse for administrators and professors is how homework solution manuals are passed around by thousands of students to their peers for numerous classes. Most of these classes are introductory classes that form the foundations of what these students will learn later so copying homework solutions really doesn't lead to learning and understanding. In the same vein, having and studying from past exams and (past) exam solutions are ethically questionable as well, especially when it's not the instructor that hands those out to students.

That's not to say these kids are bad students or don't work hard. On the contrary, many students regularly get A's in their exams and classes overall. But with students taking hard classes and more hours after that filled with multiple extracurricular activities, they rarely have the time to go through an ideal homework process. But is that chance to expedite the homework or studying process is opportunistic? Absolutely. Is it dishonest or unethical? That remains to be seen and depends on a variety of other factors, such as circumstances. It's best to examine these on a case-by-case basis. This all circulates back to the gray area between academic honesty and dishonesty - what constitutes academic integrity?

But I say all this because I want to address the point of this blog: I had a friend in high school who absolutely did not consult any solution manuals to any homework assignment and who always studied by herself to get A's on her own merit and hard work. If any of her friends or peers asked her for help, she would always be more than happy to help them conceptually but never gave them straight answers or her homework to copy. All throughout high school, I observed this fact, that even though she presumably could have used other resources, even the perfectly ethical 'office hours' after school with our teachers. As to why she never consulted outside help, I can only speculate that she was very confident in her abilities and knew it was far better to spend time to grasp concepts and do her own work. It was commendable on her part and it paid off extremely well for her - she was class valedictorian and now attends Princeton University.

I know she isn't the only person like that but she's the one that I knew. This example of opportunism is not, say, as bad as a TV drama where the vice president has the antidote to an ailment a first-term president is suffering from but does not give it to him because he wants to be the new president. I wish I had a better story to tell, something with more oomph or pizzazz but the more I think about it, the more I think that this story is appropriate because of the indelible impression it left on my mind. That hard work without looking for shortcuts pays off in the long run. There is a trade-off of the time and effort spent in the short-run but then again, long run is what matters.

Students might often collaboratively work in groups when the assignment does not call for it, and while they may not always copy each other's work word for word, it is still not strictly ethical behavior. But what is ethically worse for administrators and professors is how homework solution manuals are passed around by thousands of students to their peers for numerous classes. Most of these classes are introductory classes that form the foundations of what these students will learn later so copying homework solutions really doesn't lead to learning and understanding. In the same vein, having and studying from past exams and (past) exam solutions are ethically questionable as well, especially when it's not the instructor that hands those out to students.

That's not to say these kids are bad students or don't work hard. On the contrary, many students regularly get A's in their exams and classes overall. But with students taking hard classes and more hours after that filled with multiple extracurricular activities, they rarely have the time to go through an ideal homework process. But is that chance to expedite the homework or studying process is opportunistic? Absolutely. Is it dishonest or unethical? That remains to be seen and depends on a variety of other factors, such as circumstances. It's best to examine these on a case-by-case basis. This all circulates back to the gray area between academic honesty and dishonesty - what constitutes academic integrity?

But I say all this because I want to address the point of this blog: I had a friend in high school who absolutely did not consult any solution manuals to any homework assignment and who always studied by herself to get A's on her own merit and hard work. If any of her friends or peers asked her for help, she would always be more than happy to help them conceptually but never gave them straight answers or her homework to copy. All throughout high school, I observed this fact, that even though she presumably could have used other resources, even the perfectly ethical 'office hours' after school with our teachers. As to why she never consulted outside help, I can only speculate that she was very confident in her abilities and knew it was far better to spend time to grasp concepts and do her own work. It was commendable on her part and it paid off extremely well for her - she was class valedictorian and now attends Princeton University.

I know she isn't the only person like that but she's the one that I knew. This example of opportunism is not, say, as bad as a TV drama where the vice president has the antidote to an ailment a first-term president is suffering from but does not give it to him because he wants to be the new president. I wish I had a better story to tell, something with more oomph or pizzazz but the more I think about it, the more I think that this story is appropriate because of the indelible impression it left on my mind. That hard work without looking for shortcuts pays off in the long run. There is a trade-off of the time and effort spent in the short-run but then again, long run is what matters.

Wednesday, September 11, 2013

Ronald Coase - One of the Greatest Economists

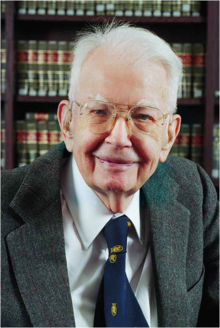

Ronald Coase

Ronald Coase was a British-born American economist who won the 1991 Nobel Prize in Economics for his significant work in transactions costs and property rights in the functioning of the economy (Coase Institute). Born on December 29, 1910, Mr. Coase attended the University of London and the London School of Economics, where he got his Bachelor's degree. He worked at LSE for fifteen years before moving to the University of Buffalo in the mid-1950s. After a brief stint at the University of Virginia from 1958 to 1964, he moved to the University of Chicago, where he was the Clifton R. Musser Professor Emeritus of Economics, and stayed as a distinguished faculty member for the rest of his academic career.

Mr. Coase's work was influential for many reasons but he is especially known for these two: transactions costs of the firm, and how property rights could overcome externalities. The first, he published when he was only 26 years old, in a paper titled "The Nature of the Firm" (1937). In this seminal piece, Mr. Coase tries to explain why people choose to organize themselves into business firms rather than each contracting out the work for themselves. Coase's main explanation for this is that there are various transactions costs related to functioning in the open market that are eliminated when people create companies instead of subcontracting. For example, a certain person and his subcontractor would need to spend time bartering before agreeing on a price and this hassle is stricken through the organization of corporations, where many jobs and functions can be performed in-house.

The second reason, involving property rights, Coase published in a paper named "The Problem of Social Cost" (1960) in the Journal of Law and Economics while he was a faculty member at the University of Virginia. In this paper, Coase writes that it is unclear where the blame for externalities or negative consequences lie. He concludes that is important that the government clearly define property rights so that the question of who, in an economic scenario involving two or more parties, is the more harmed by a certain choice or action. In his words, "the problem is to avoid the more serious harm". Together with sufficient transaction costs, initial property rights matter for both equity and efficiency.

This leads to the famous "Coase Theorem" which is associated closely with Ronald Coase, who said that the theorem, taken from a few pages of his "The Problem of Social Cost" paper, was not about his work at all. Even though Coase said in his paper that property rights should be well defined, the Coase Theorem posits that if trade in an externality is possible and there are no transaction costs, then bargaining will lead to an efficient outcome regardless of the initial allocation of property (Wikipedia). In essence, involved parties don't have to consider how property rights are granted so long as they can negotiate and trade to produce a mutually advantageous outcome. His 1960 paper, however, argues that since transactions costs are rarely low enough to produce such an efficient outcome, the theorem is not applicable to economic reality.

Before reading about Mr. Coase in the New York Times last week, I knew nothing about him. I certainly did not know he was a Nobel Prize winner and such an esteemed luminary in the field of economics. Mr. Coase contributed a great deal and amount of research, and was arguably one of the greatest economists of the twentieth century. His inadvertent creation of the Coase Theorem has led to countless papers and research in the subfields of perfect competition, game theory, and the economics of government regulation. His work on transactions costs, social costs, and especially the nature of the firm, will be highly relevant to our class since we do talk about the economics of organizations. Ronald Coase died on September 2, 2013, at the age of 102.

Subscribe to:

Posts (Atom)